Regime change for the dollar?

With the tariff policy unveiled on Liberation Day on 2 April, the Trump administration intends to rebalance world trade and in particular to reduce the US trade deficit. This project therefore goes beyond the simple framework of trade disputes with a country or a group of countries and, as we shall see, it calls into question the place of the dollar in the global economic and financial system.

Published on 2 May 2025

Some theoretical reminders on the valuation of currencies

With the tariff policy unveiled on Liberation Day on 2 April, the Trump administration intends to rebalance world trade and in particular to reduce the US trade deficit. This project therefore goes beyond the simple framework of trade disputes with a country or a group of countries and, as we shall see, it calls into question the place of the dollar in the global economic and financial system.

In the Fundamental Equilibrium Exchange Rate (TEER) equilibrium models, it is assumed that a country with a current account deficit (or a current account surplus) that is too high has an overvalued (or undervalued) currency and that this currency must depreciate (or appreciate). The major disadvantage of these models is that they are prescriptive and it is not clear at what threshold a current account surplus or deficit is excessive. In any case, it can be noted here that the absorption of a deficit that is too high (or ... considered too high) requires a depreciation of the currency.

In a family of later models, the Behavorial Equilibrium Exchange Rate (BEER) models, the empirical relationships between the effective real exchange rate and certain economic variables are considered. One of the most widely used variables is the terms of trade, i.e. the ratio of export prices to import prices: this variable is particularly relevant for countries that import or export a lot of raw materials. The currency of a commodity- exporting (or importing) country whose price is rising tends to appreciate (or depreciate).

The United States has a current account deficit considered too high by the new American administration and theoretical models consider that the depreciation of the dollar would be necessary to reduce it. In a previous text, we concluded that "reducing US trade deficits without weakening the dollar seems very complicated". In addition, the United States has gone from being a massive importer of gas and oil for decades to an exporter of fossil products. As a result, the US administration's desire to lower gas and oil prices implicitly corresponds to the desire for a deterioration in the terms of trade and therefore also to a depreciation of the dollar.

The accumulation of trade deficits has led to massive indebtedness to the rest of the world: this is a key factorin the value of Treasury securities

A country with a current account deficit (or current account surplus) becomes a debtor (resp. creditor) of the rest of the world, i.e. it is indebted to the rest of the world. Thus, current account deficits (resp. current account surpluses) are generally associated with inward financial flows (resp. outgoing members). In the balance of payments, which lists all transactions between residents and non- residents, the current account and the financial account should theoretically balance each other.

Since the early 1980s, the United States has only had a brief current account surplus in 1991 (the country was in recession) and has always been in a current account deficit otherwise. This accumulation of current account deficits by the United States over decades has caused this country to become extremely indebted to the rest of the world, with a net external position indebted to 88% of its GDP at the end of 2024. These current account deficits have been financed almost entirely by portfolio investment flows, i.e. by purchases by foreigners of US financial securities. And even though attention has often been turned to the equity markets and in particular to the Magnificent Seven, the vast majority of US securities bought by non-residents have been debt securities (87% over the ten years from 2015 to 2024). Among the long- term debt securities, there are obviously many Treasury securities but also corporate bonds. Ultimately, the accumulation of current account deficits by the United States has led this country to borrow from the rest of the world in large part by selling Treasury securities. As we shall see in the rest of this text, the substantial accumulation of dollar reserves by many emerging countries and the fact that the dollar is the dominant currency are consubstantial with this mechanism.

We can recall the famous "conundrum" evoked by former Fed Chairman Alan Greenspan during the 2000s: at the time, US long-term rates were artificially compressed by the size of foreign purchases of Treasury securities, which was itself the mirror of a historically high current account deficit (around 6% of GDP in 2006).

As a result, the possible reduction of the US trade deficit would be offset by a sharp decline in demand for US bonds from the rest of the world. As we shall see, this perspective also raises questions about the role of the dollar inglobal economic and financial systems.

Fordecades, the dollar has been central to foreign exchange reserve

Foreign exchange reserves are assets held by central banks or government entities in foreign currencies or gold. Foreign exchange reserves provide a country with sufficient liquidity to conduct foreign exchange transactions if necessary, for example to ensure a rigid or flexible peg to a reference currency (this is most often the dollar, but it can be the euro or other currencies).

Emerging market economies sharply increased their foreign exchange reserves in the aftermath of the Asian crisis of the late 1990s, when it became clear that they needed to hold enough foreign currency, especially dollars, to cope with a sharp withdrawal of foreign investment. Other countries, and in particular China, have accumulated dollars for an extended period of time in order to prevent their currencies from appreciating and to remain competitive. Again, it should be remembered that the accumulation of foreign exchange reserves in dollars would not have been possible without the accumulation of current account deficits by the United States.

The choice of the distribution of foreign exchange reserves has been a subject of academic research in its own right for decades. The dollar has been the dominant currency since the Second World War and it has been by far the most used currency in the world's foreign exchange reserves since that period. The allocation of reserves in the different currencies depends on the country. It is generally accepted that the weight of the dollar in reserves is higher in countries where a large share of exports are denominated in dollars or in countries whose currencies fluctuate less against the dollar than against other key currencies1.

IMFdata show that the dollar's share of the $12300 billion in global foreign exchange reserves was still 58% at the end of 2024, after a slight downward trend in recent years (61% at the end of 2019). This decline can be explained by the fact that somecountries that have experienced diplomatic tensions with the United States in recent years have at least reduced the share of the dollar in foreign exchange reserves in favor of other currencies. In addition, thefinancial sanctions decided in recent years by Western countries havealso caused a diversification against Western currencies and in favour of gold2 (the volumes of gold held by central banks have increased by 20% since the end of 2008).

Thefact that countries with large foreign exchange reserves continue to give the dollar an important place in them (which is a determining variable for the demand for dollars) actually raises the question of whether or not the dollar can remain the dominant currency in trade and financial exchanges.

Can the dollar remain the dominant currency?

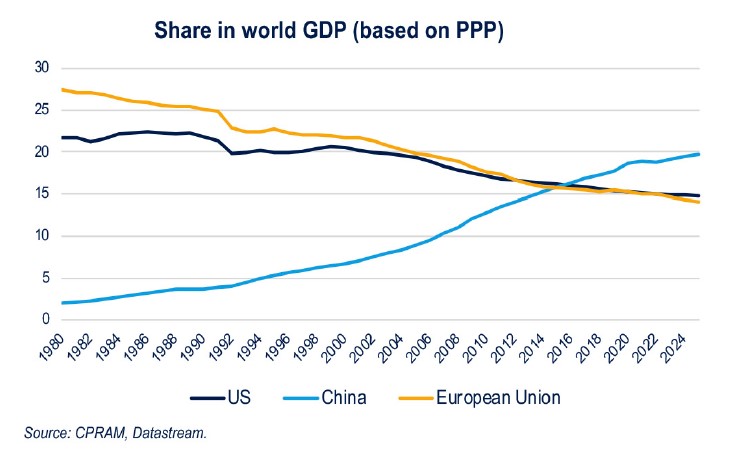

The question of whether the dollar can remain the dominant currency in the international economic and financial systems has been a recurring one for years, especially since the United States accounted for only 15% of global GDP3 in 2024, i.e. less than China (around 20%) while it was far above any other country a few decades ago.

With the birth of the euro in 1999 and the emergence of the Chinese economy, the end of the dollar's hegemony has been predicted many times. However, the American currency remains the dominant currency as was the pound sterling in the nineteenth century and the beginning of the twentieth century. Economists generally summarize the attributes of the dominant currency as follows4:

- it is used preferentially for the invoicing of international commercial transactions and foreign banks must be able to finance themselves easily in it, in order to be able to lend to their customers, and foreign companies can borrow directly in it,

- for these reasons, it is the currency against which foreign central banks try to stabilize their own currencies, and it is mainly in this currency that they accumulate their foreign exchange reserves.

- As the safest currency, international private investors overweight financial assets denominated in this currency.

This helps to understand why the dollar's hegemony has not been radically challenged so far. The Chinese currency, the renminbi, is a potential competitor currency, but the fact that capital controls remain and that it is not easy to finance oneself in this currency are very important obstacles to it becoming a dominant currency in the years to come. Economist Barry Eichengreen5 points to another difficulty for the internationalization of the renminbi: since the early 19th century, the dominant currencies have been those of countries with democratic systems with checks on the executive branch and where creditors were strongly protected. The euro is another potential competitor but the weight of the euro zone is declining and weaker than that of the United States... The same goes for the yen, which is currently the 3rd most used currency in foreign exchange reserves.

The unpredictability of the new US administration and the recurrent threats weaken the dollar's status as the dominant currency and may in itself cause a decline in its international use. However, there is currently no other currency capable of replacing it.

The impact of tariffs on the foreign exchange market: is this time different?

Academic research6 generally notes that countries that implement tariff increases see their currencies appreciate. This is what we saw in particular during the trade war of the first Trump administration in 2018/2019. Following Donald Trump's victory in the November 2024 election, the dollar appreciated in part due to the anticipation of tariff hikes. However, the dollar has depreciated sharply since Liberation Day on April 2 (announcements of much higher and broader-than-expected tariff increases).

Two hypotheses can be formulated:

- the much sharper-than-expected tariff hikes increased the likelihood of a US recession, which weighed heavily on the dollar,

- The plan unveiled on April 2 goes beyond simple tariff increases against a country or a group of countries and aims to reduce the United States' trade deficit, i.e. the highest trade deficit in the world and which is also that of the country of the dominant currency, whatever the cost. This has probably eroded at least a little bit the dollar's status as the dominant currency and led some central banks to reduce its weight in their foreign exchange reserves in favor of the euro, the yen and gold.

Conclusion

The general conclusion is that the plan unveiled on 2 April to reduce the US trade deficit at all costs is likely to at least slightly undermine the dollar's status as the dominant currency, since formany countries, the decline in dollar-denominated exports will reduce the interest in having dollar foreign exchange reserves. The unpredictability of the new US administration and the recurrent threats also weaken the dollar's status as the dominant currency and may in itself cause a decline in its international use. Nevertheless, the dollar is not expected to lose its status as the dominant currency overnight, mainly because there is currently no other currency capable of replacing it.

On the trade front, the fact that the new US administration wants to put an end to a current account deficit that is considered too high requires a depreciation of the dollar. Moreover, the desire to lower gas and oil prices implicitly corresponds to the desire for a deterioration in the terms of trade and therefore also to a depreciation of the dollar.

1. See for example Ito H. t R. McCauley, 2019, "The currency composition of foreign exchange reserves", BIS working paper.

2. Arslanalp S., B. Eichengreen et C. Simpson-Bell, 2023, ” Gold as International Reserves: A Barbarous Relic No More?”, IMF working paper.

2. GDP considered in purchasing power parity. IMF figures.

4. See Gopinath G. and J. Stein, 2020, "Banking, Trade, and the Making of a Dominant

Currency", Quarterly Journal of Economics, or Gourinchas P.-O., 2019, "The Dollar Hegemon? Evidence and Implications for Policy Makers"

5. Eichengreen B., 2013, « Number One Country, Number One Currency? », The World Economy, vol. 36, no 4.

6. Furceri D., H. Swarnali, J. Ostry et A. Rose, 2019, “Macroeconomic Consequences of Tariffs”, IMF working paper.